It’s no secret that buying a car is more expensive today than it was three years ago. New car price trends reveal that the average new vehicle payment with a five-year loan hit $736 in the third quarter of 2023 – an all-time high. More than one in six buyers currently pay more than $1,000 per month.

There are a myriad of reasons for this jump—residual supply-chain-driven inventory shortages for some models and trims, high-interest rates that still exceed 7% even with the best consumer credit ratings (and above 10% for those with lower ratings), and the discontinuation or reduced production priority for lower priced models, among others. These factors push many would-be buyers out of the market or force them to make compromises on their choices.

Let’s look at a few of these factors in more detail.

Interest Rates

Immediately after the pandemic and throughout 2021, Federal Reserve policy was oriented around managing economic recovery, and interest rates remained historically low. But starting in the spring of 2022, that policy shifted to combat inflation, and a series of hikes ensued, pushing auto loan rates up.

Source: Statista.com

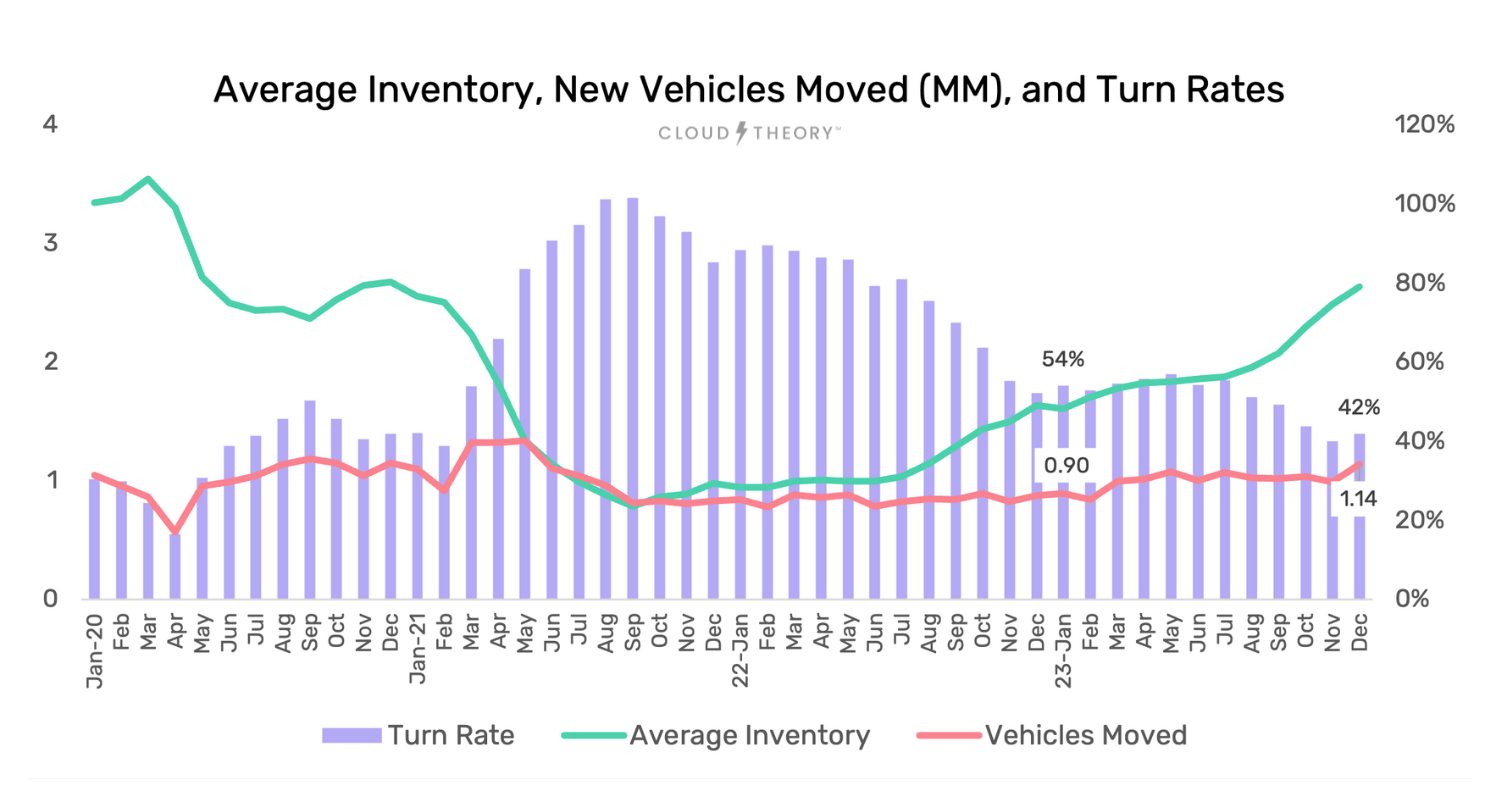

Inventory

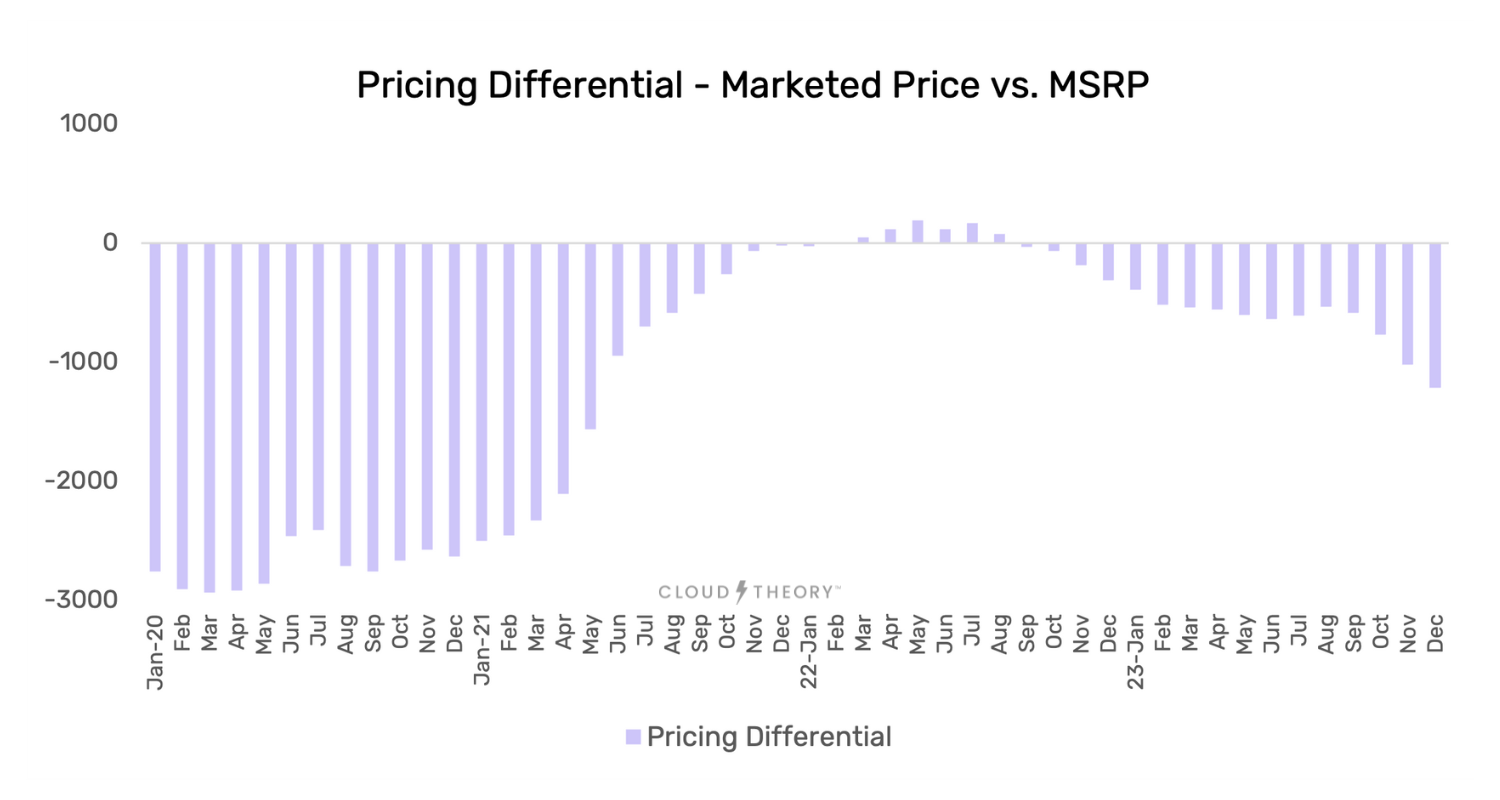

Meanwhile, inventory declines—initially by chip shortages and later by broader supply chain issues—drove turn rates up dramatically and marketed prices above MSRP in late 2021 and throughout most of 2022 as demand ruled the day. While those trends eased in 2023, they have not returned to pre-pandemic levels.

(Pricing Differential Above 0 Indicates Car Prices Were Marketed Above MSRP)

Model Selection

In 2019, there were 44 vehicles with marketed prices below $25,000 and 28 more priced between $25,000 and $30,000. Collectively, these vehicles represented an average inventory level of 1,290,000. Four years later, thirteen of those vehicles were discontinued, and the inventory available for the remaining ones was 442,000—down almost two-thirds. And many of them were priced well above $30,000.

In fact, the number of vehicle choices being marketed below $30,000 was just 19, with a total amount of inventory of 145,000 in 2023—down almost 90% from four years earlier.

Impact on Consumers

To put this all into perspective, many financial experts recommend a car payment of roughly 10% of household take-home pay. With an average payment of $736 per month, this translates to a net income level of $88,000, or roughly $120,000 in gross income. According to the latest income statistics, less than one-third of households are at that level.

So, where do OEMs go from here? There are signs on multiple fronts that prices hit their peak in 2023 and multiple factors that will apply some level of gravity in 2024. The Fed has signaled that it will likely ease interest rates, though slowly and most likely in the back half of the year. And accelerating inventories, coupled with relatively static demand, are applying pricing pressure and an increased reliance on incentives.

But there is little doubt that prices will remain elevated and consumer choices at the lower end will remain much more limited than before. With all that said, OEMs will have to carefully navigate continuing economic challenges among consumers and balance their own economic considerations. Management of incentives, expansion of leasing programs to reduce monthly payments, and a greater emphasis on producing base or mid-level trims are some strategies and tactics that will need to come into play.

OEMs that monitor inventory supply and consumer demand relative to competitors will also be able to refine their pricing more effectively. Models with relatively high supply and low demand in one geographic market will need more aggressive pricing actions than a market in the opposite situation. A real-time view of the marketplace on a granular geographical level will enable smart incentive (and marketing) allocations to better compete in the areas that need it most.

.jpg?width=300&height=175&name=Shutterstock_676056058%20(1).jpg)